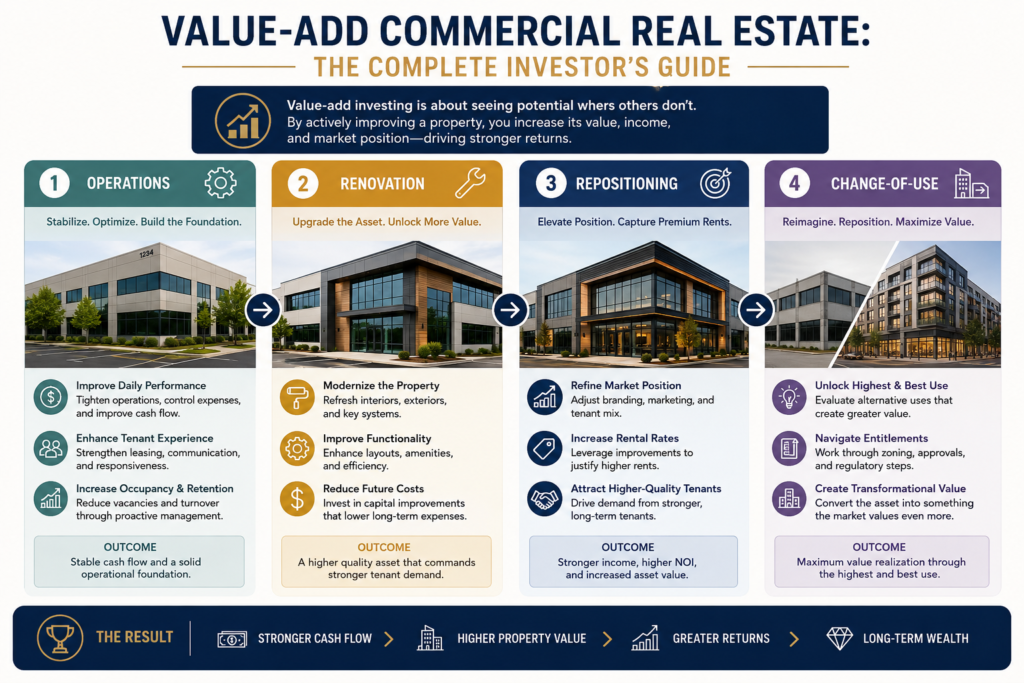

Value-Add Commercial Real Estate: The Complete Investor’s Guide

There is no one-size-fits-all path in commercial real estate investment. Some investors want stable income, while others want higher returns and accept more moving parts. Value-add commercial real estate sits between those poles.

The strategy is simple at first glance: you buy an underperforming asset, improve it, increase income, and sell or refinance at a higher value. This guide digs deeper and explains what value-add real estate means, how sponsors create value, where the risk sits, and how a sample deal works.

What Value-Add Means in Commercial Real Estate

Value-add real estate is a strategy built around a fixable gap. The property already exists, usually produces some cash flow, and often has zoning, legal use, and infrastructure in place. But it’s not performing as well as it could.

This gap may come from the building, leases, tenant mix, costs, or management. The investor’s job is to find a property where the fix costs less than the value it creates.

The underperforming-asset thesis

In value-add real estate investing, the sponsor buys a commercial property with room to increase its value through physical improvements, operational changes, or both. The target is not a perfect asset but rather a property where better execution can turn existing square footage into higher income and asset value.

A building may underperform because it is:

- Dated

- Carrying deferred maintenance

- Missing the amenities tenants now expect

It may have high vacancy, below-market rents, weak leasing, poor property management, or an owner that lacks capital. In each case, current property value doesn’t reflect the income the asset could produce after value creation work is complete.

Light vs. heavy value-add

- Light value-add is a refresh. In multifamily, light work might mean paint, flooring, lighting, landscaping, and better common areas.

- Heavy value-add is closer to gut-to-the-studs. It can be full unit renovations, new amenities, structural reconfiguration, or major systems work. In office buildings, heavy projects may include re-skinning the façade, reworking floor plates, or modernizing the building for a different tenant profile.

The Value-Add Business Plan: How Sponsors Create Value

The business plan is the heart of value-add investing. Just buying a building and hoping the market lifts it is not the way to do it. Sponsors are underwriting specific actions that should change the property’s income profile.

These actions usually fall into three buckets:

- Increase revenue.

- Reduce waste.

- Improve market perception.

The best plans connect every capital dollar to a measurable result:

- Higher rents

- Better occupancy

- Lower expenses

- A stronger buyer pool at exit

Net operating income is the engine

Net operating income, or NOI, is the property’s income after operating expenses but before debt service and taxes. In other words, it’s the cash flow the real estate itself produces. Value-add projects focus on NOI because commercial property value is usually tied to income.

The common formula is:

Example: If a property produces $500,000 in NOI and sells at a 5% cap rate, its value is roughly $10 million. Raise NOI to $650,000 at the same cap rate, and the implied value becomes $13 million. That’s why NOI growth is the engine. It’s also where sponsor-driven alpha comes from: the return is created by asset-level execution, not just market movement.

Physical improvements

Physical improvements only count when they help the property earn more or lease faster.

- Renovated apartment units can support higher rents

- Better lobbies, corridors, fitness rooms, outdoor areas, parking, signage, and landscaping can make a property easier to lease

- Energy-efficient upgrades may reduce costs or attract sustainability-focused tenants

The point is to spend where the improvement can translate into rent, occupancy, retention, or lower expenses. Just making a building prettier won’t cut it.

Operational improvements and lease-up

Not every value-add plan starts with construction. Sometimes the fastest upside comes from better operations:

- Replacing the property manager

- Tightening expenses

- Improving leasing discipline

- Changing vendor contracts

- Shifting more costs to tenants through triple-net lease structures where appropriate

A logical progression is operations first, then renovation, then repositioning, then change-of-use.

- Operations stabilize the basics

- Renovation improves the product

- Repositioning changes the tenant pool.

Change-of-use is the most aggressive version and can start to resemble opportunistic investing.

In a classic value-add plan, the sponsor renovates, leases vacant space, improves the tenant mix, stabilizes cash flow, and exits at a higher value.

Where Value-Add Sits on the Risk-Return Spectrum

СКУ strategies are usually grouped into core, core plus, value-add, and opportunistic. The categories describe risk, required execution, and where returns are expected to come from.

Value-add sits in the middle. It’s riskier than buying a fully leased, institutional-quality asset, but usually less complex than building from raw land or converting a property to a new use.

Core and core plus

- Core investments are the income stocks of CRE. They’re typically stabilized, high-quality properties in strong locations, with creditworthy tenants and predictable cash flow.

- Core plus is more like growth-and-income: still income-oriented, but with some room for improvement, modest leasing risk, or a slightly less prime location.

These strategies usually prioritize durability over dramatic upside.

Value-add vs. opportunistic

People tend to lump Value-add and opportunistic investments together, but they’re not the same.

- Value-add usually means improving an existing, permitted property. The building is there, the legal use generally exists, so the sponsor is trying to raise income through renovation, management, lease-up, and repositioning.

- Opportunistic strategies sit further out on the risk curve. They may involve ground-up development, raw land, major distress, or a true change-of-use conversion. These projects can take years before producing income, and entitlement delays might damage returns before construction begins.

The key advantage of value-add is that the investor is working with an existing asset, which can reduce entitlement risk compared with building from scratch.

Leverage, Returns, and Risk

As a current benchmark, Verus’ 2026 capital market assumptions model value-add real estate at a 9.2% nominal 10-year return, about 200 basis points above core real estate. Older CBRE Investment Management research put value-add net return targets higher, around 11–13%, with typical leverage of 50–70% and income contributing 30–60% of total return.

The gap between these numbers tell us something: in the current higher-rate market, investors still expect a premium for value-add risk, but the premium has to be earned through execution, not cheap debt.

The building blocks are in-place income, NOI growth, leverage, and cap-rate movement. Leverage can boost returns, but it also magnifies mistakes. Cap-rate expansion is the biggest threat: if exit cap rates move higher, the same NOI is worth less. Conservative sponsors underwrite flat-to-expanding exit cap rates, maintain enough income to carry the asset, use moderate leverage, and avoid plans that depend entirely on a perfect sale market.

| Return/risk factor | Role in a value-add deal | Why you should care |

| In-place income | Existing rent and occupancy at acquisition | Helps carry the asset while renovations and lease-up are underway |

| NOI growth | Higher net operating income from rent increases, better occupancy, and expense control | The main value-creation driver, because property value is tied to NOI |

| Leverage | Debt used to finance the acquisition and improvement plan | Can boost returns, but also increases risk if costs rise or lease-up is slower than expected |

| Cap-rate movement | The exit valuation multiple applied to stabilized NOI | A higher exit cap rate can reduce value even if NOI improves |

| Income share of return | The portion of total return coming from cash flow rather than sale gain | More income can create downside protection if the exit market weakens |

A Sample Value-Add Deal

Take a look at a simple multifamily example:

A sponsor buys a 100-unit Class C apartment property for $10 million:

- The asset is 86% occupied

- Average rent is $1,050 per month

- Annual NOI is about $520,000

- The purchase cap rate is 5.2%

- The property is dated, but the location is solid and renovated competitors achieve higher rents

The sponsor budgets $1.5 million for improvements over three years:

- $12,000 per unit for 75 units as they turn over

- Plus common-area upgrades, exterior repairs, signage, landscaping, and a leasing refresh

After renovation, average rent rises by $225 per renovated unit, occupancy improves to 94%, and better management cuts operating leakage. By year four, NOI reaches about $760,000.

If the stabilized property sells at a 5.5% cap rate, the exit value is roughly $13.8 million. Total basis is $11.5 million before financing and transaction costs, so the plan creates about $2.3 million of gross value. If the exit cap rate is 6.0%, the same NOI supports a value closer to $12.7 million.

How to Invest and Vet a Sponsor

Investors can pursue value-add opportunities actively or passively.

- Active investors may act as the sponsor, buy through a joint venture, source deals from brokers, pursue off-market owners, or search commercial real estate listings for under-managed assets. This route requires capital, relationships, underwriting skill, and execution capacity.

- Most passive real estate investors are better served as limited partners in a syndication, fund, or REIT led by an experienced sponsor. Due diligence should focus on the sponsor’s track record, net worth, capital at risk, financing plan, renovation budget, lease-up assumptions, exit cap rate, reserves, and evidence that the plan fits the market.

Conclusion

Value-add CRE investing can be profitable, but it rewards execution more than optimism.

It’s not better or worse than core, core plus, or opportunistic CRE. It’s simply a different risk profile. Investors should match value-add strategies to their goals, risk tolerance, and time horizon, then study the sponsor as carefully as the asset.

Editor’s note: This material is educational, not investment advice.