How to Buy a Strip Mall: Complete 2025 Investment Guide

Headlines consistently predict the retail’s decline, yet experienced investors can always spot an opportunity. Strip malls frequently written off as outdated commercial assets – have proven remarkably resilient. Their survival stems not from competing with online stores but from housing businesses that require physical presence: you cannot get a haircut through your phone or pick up a takeout from a warehouse. Makes strip malls an evergreen investment with steady cash flow and long-term growth potential, regardless of the e-commerce upsurge.

The Investment Thesis: Why Buy a Strip Mall?

Strip malls deliver dual returns that set them apart in commercial real estate. These local hot spots generate reliable income thanks to diverse tenants while offering moderate appreciation tied to local population growth and suburban development. Most established markets provide current yields between 6-8 percent with annual appreciation potential of 3-5%; total returns comparable to institutional assets but accessible to individual investors.

The Service-Oriented Tenant Framework

Strip malls rely on businesses that e-commerce can’t replace. Key categories include beauty salons , fast-casual restaurants, medical offices like dentists or opticians, and essential services such as dry cleaners. Targeting tenants that require physical presence and stable foot traffic secures the strip malls’ position without putting it into competition with online retail trends.

Strategic Property Specification Advantages

Smart investors find value in standardized layouts rather than specialized designs. Flexible infrastructure accommodates various types of businesses without costly renovations. This approach broadens the tenant pool, speeds up leasing during vacancies, and lowers capital reserve needs – improving net operating income stability over time. The numbers show this strategy directly supports stronger property valuations.

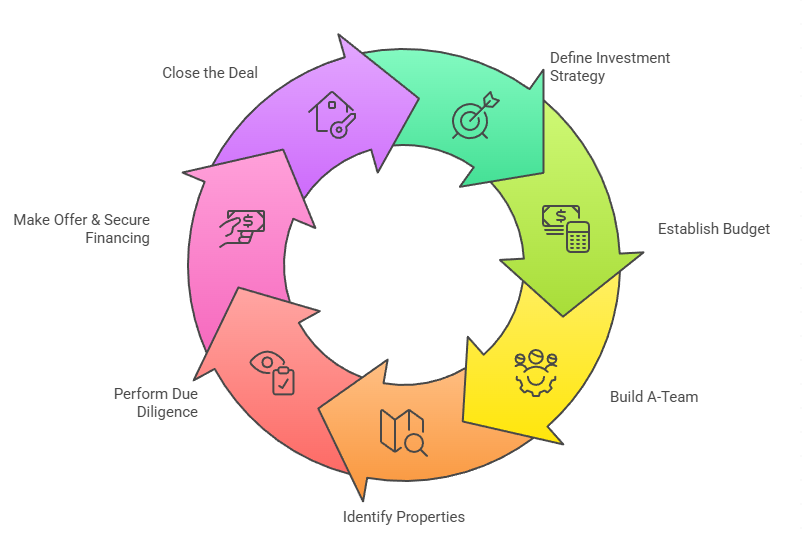

Your Acquisition Playbook: Step-by-Step Guide

Moving from theory to action requires careful consideration of financial, legal, and operational factors. This guide will help you navigate a strip mall acquisition with more confidence and experience.

Step 1: Define Your Investment Strategy & Goals

Clear strategy precedes property search in successful commercial real estate deals. Determine whether you seek passive income from stable assets or value-add opportunities through renovations and re-leasing. The former favors properties with established tenants and predictable income, while the latter targets underperforming assets where improvements may boost returns.

Your strategy shapes acquisition criteria and time horizon. Cash flow investors prioritize markets with stable rents and dense populations. Value-add seekers evaluate local job growth, economic diversity, and competitive supply. Risk tolerance completes this foundation. Conservative investors prefer mature suburban areas with varied employers, while aggressive buyers may pursue high-growth markets with greater execution risk.

Step 2: Establish Your Budget & Funding Plan

Comprehensive planning extends beyond purchase price to include all transaction costs and reserves. Budget for the property cost, down payments (typically 20-30% of purchase value), closing costs of 2-4%, and capital reserves for repairs or tenant improvements. Experienced buyers also set aside funds for leasing expenses like tenant allowances and commissions.

Financing structure significantly impacts returns. Most strip mall deals combine investor capital with CRE loans. Traditional CRE financing offers 70-80% loan-to-value ratios with 20-25 year terms, though conditions vary by property quality and borrower strength. Owner-occupants using over 50 percent of the space may qualify for Small Business Administration loans, which provide lower down payments and longer amortization periods, improving cash-on-cash returns.

Getting lender pre-approval before making offers gives you a competitive edge. It demonstrates financial capability to sellers and reveals potential financing hurdles early. This step separates serious buyers from casual bidders.

Step 3: Build Your Professional “A-Team”

Strip mall acquisitions require specialized expertise to avoid costly mistakes. Your core team should include:

- Commercial brokers with retail property experience to identify opportunities and negotiate terms

- Real estate attorneys to review contracts and ensure legal compliance

- Commercial accountants to advise on tax strategies and entity structure

- Property inspectors to assess physical structure and systems conditions

- Commercial lenders to structure appropriate financing

Allowing domain experts to evaluate a property will ensure you know exactly what you invest in.

Step 4: Identify & Analyze Suitable Properties

Property screening starts with three main factors: location, tenant quality, and physical condition. High-traffic positioning with good visibility and easy access drives tenant demand. Diverse, stable tenants with strong leases provide income reliability. Minimal deferred maintenance reduces immediate capital needs.

Look beyond public listings. Platforms like Realmo show available properties, but brokers often control off-market deals. Focus on densely populated urban and suburban areas with diverse job markets. These locations typically weather economic shifts better than areas dependent on single employers. Demographic stability usually matters more than market timing for long-term success.

Step 5: Perform Rigorous Due Diligence

Perform a rigorous check of all seller claims to uncover hidden risks and avoid problems after closing the deal.

Financial analysis centers on NOI – revenue after operating expenses but before debt payments. Scrutinize historical income statements and project future cash flow to reveal whether the price matches market value and projected returns.

Lease review is critical for income properties. Examine rental rates against market comparables, lease expiration dates, renewal options, and rent increases. Triple net leases (NNN) – where tenants cover operating expenses – typically deliver better returns than gross leases.

Physical inspections by qualified professionals evaluate structural integrity, roofing, HVAC, electrical systems, and parking conditions. This assessment creates capital expenditure budgets for immediate repairs and future replacements.

The rent roll documents current tenants, rates, and lease terms. Staggered expirations prevent simultaneous vacancies that devastate cash flow. Direct tenant conversations add context you won’t find in documents, revealing satisfaction levels and renewal intentions.

Step 6: Make an Offer & Secure Financing

Once you’re certain about the investment, work with your broker and attorney to structure a competitive offer. Include purchase price based on NOI analysis, inspection and financing contingencies, and realistic closing timelines.

Advance financing applications simultaneously with your offer. Provide lenders with rent rolls, operating statements, leases, and inspection reports. They will conduct independent appraisals and underwriting. Don’t forget to carefully evaluate interest rates, loan terms, and prepayment penalties as they significantly impact long-term returns.

Having preapproval documentation and professional teams can gain you negotiation advantages.

Step 7: Close the Deal

Closing requires one last coordinated team effort. A final walkthrough confirms no tenant departures or major issues since due diligence. Attorneys handle legal document signing, title transfer, and fund coordination. Buyers transfer funds while lenders disburse loans. Investors get ready to take ownership and begin managing operations.

The Financials: Valuation, Costs & Profitability

How to Value a Strip Mall: The Capitalization Rate Method

Commercial real estate uses several valuation methods, but the capitalization rate (cap rate) approach is best for comparing income-producing properties. It relates annual net operating income to market value – similar to dividend yields in stock investing.

The Cap Rate Valuation Formula

The calculation is straightforward: Property Value = Annual NOI ÷ Cap Rate. For example, a 12,000 sq ft strip mall generating $360,000 in annual NOI at a 5% cap rate is valued at $7.2 million ($360,000 ÷ 0.05 = $7,200,000). Investors use this formula to both set purchase prices and calculate implied cap rates from asking prices.

Cap Rate Market Dynamics and Valuation Impact

Cap rates shift with market conditions, interest rates, and property risks, creating major valuation differences for identical cash flows. That same $360,000 NOI property at an 8% cap rate (reflecting higher risk) values at $4.5 million ($360,000 ÷ 0.08). This $2.7 million difference shows how market sentiment directly affects investment value. Timing and accurate cap rate assessment become critical.

Development Economics: Ground-Up Construction Costs

New strip mall construction typically costs between $2.5-$3.5 million for a 12,000 sq ft property. This includes land acquisition, construction at $200-$300 per square foot, site work, parking, and initial tenant improvements. While offering design control, development introduces construction risk and extended lease-up periods before stable cash flow begins.

Acquisition Price Spectrum for Existing Properties

Existing strip malls show extreme price variation based on location, tenant quality, condition, and local economics. Distressed properties in tertiary markets may list below $135,000, while premium neighborhood centers in growing areas can expect to fetch $22 million or more. Investors should compare values per square foot and cap rates rather than absolute prices.

Revenue Fundamentals: National Rental Rate Benchmarks

Rental income averages $22 per square foot annually across U.S. markets, though rates vary significantly. Urban and affluent suburban areas often exceed $30 per square foot, while secondary markets may yield $15-$18. Local rental trends and competitive supply pipelines prove essential for projecting income.

The Profitability Reality: Operational Margin Analysis

Strip mall ownership presents challenging economics due to relatively thin margins which leave little room for dealing with tenant departures or major repairs like parking lot replacement. Properties with significant debt face particular vulnerability – losing an anchor tenant generating 30-40% of NOI can quickly turn cash flow positive assets into money-losers.

Understanding Accounting Losses vs Economic Cash Flow

Financial statements often show accounting losses during early ownership despite positive economic performance. High financing costs combined with depreciation (a non-cash charge) frequently produce reported losses even when properties generate cash flow. Experienced investors focus on EBITDA and actual cash distributions rather than net income. Properties with 78% EBITDA margins achieving cash flow breakeven by year three show strong fundamentals despite technical accounting losses – a common pattern for leveraged real estate.

Post-Purchase: Managing Your Asset

Acquisition is just the initial part of the investment cycle – it’s the ongoing operational excellence that determines whether properties meet financial success.

Four Pillars of Effective Property Management

Successful operations rely on four factors:

- Tenant relations: Proactive communication and strategic lease renewals minimize turnover costs

- Maintenance protocols: Prompt repairs prevent minor issues from becoming major expenses

- Marketing strategies: Targeted outreach fills vacancies efficiently

- Financial tracking: Monitors income, expenses, and budget variances against projections

Triple Net Lease Structure: Operational Cost Transfer Mechanism

NNN leases transfer operating expenses to tenants. Under NNN arrangements, occupants pay their share of property insurance, utilities, maintenance, taxes, and repairs along with base rent. This protects landlords from expense inflation and creates more predictable cash flow than gross leases.

Property Management Structure: Build vs Buy

Investors can choose between self-management and professional management.. Self-management saves fees – potentially $25,000+ annually – but requires time, expertise, and physical presence. Professional managers provide leasing expertise, vendor networks, and emergency response systems justifying their fees through operational efficiency. The choice should depend on your location, experience, portfolio size, and desired involvement.

The Alternative Path: Investing Without Buying

Capital Barriers and Accessibility Constraints

Direct strip mall acquisition requires substantial capital plus operational expertise. It also concentrates risk in single properties vulnerable to local downturns or tenant failures. This creates a barrier to many investors.

Real Estate Investment Trusts: Democratized Commercial Property Access

Real Estate Investment Trusts (REITs) offer commercial property exposure through publicly traded shares. These companies own income-producing real estate, distributing at least 90% of taxable income to shareholders as dividends. Shopping center REITs provide instant diversification across hundreds of properties, eliminating management responsibilities and single-asset risks.

Implementation Framework & Investment Vehicles

Investors can add strip malls to their portfolio through established REITs like Kimco Realty (KIM), operating about 500 centers nationwide, and Regency Centers (REG), focusing on grocery-anchored centers in affluent suburbs. These trusts offer daily liquidity, SEC-mandated transparency, and professional management. While REITs sacrifice direct control over properties, they avoid transaction costs and illiquidity issues of direct ownership.

Your Next Step in Commercial Real Estate

Strip mall investment remains lucrative despite retail transformation trends. Service-oriented physical businesses create sustainable cash flow. Success depends on three fundamentals: acquiring properties in demographically stable locations with proven traffic, building tenant rosters with long-term occupants, and conducting thorough due diligence to uncover hidden risks.

Begin by assembling your acquisition team – find commercial brokers with retail experience, engage specialized attorneys, and establish commercial lending relationships. Develop financial models with realistic budgets, financing structures, and capital reserves. These steps position you to act when opportunities emerge, turning knowledge into tangible wealth-building assets.

Disclaimer: The information presented in this article is for general educational purposes only and does not constitute financial, legal, or tax advice. Realmo.com assumes no responsibility for errors, omissions, or actions taken based on this content. This material should not be relied upon as a substitute for a consultation with professional advisors. Please note that laws and regulations may vary significantly by state