The Ultimate Real Estate Listing Checklist Template: Everything You Need to Attract Buyers and Close Faster

A listing is the asset’s first interaction with the market. A serious buyer approaches it looking for clarity, consistency, and possible risks. That’s what brokers should provide if they want successful deals.

This guide provides a structured pre-listing checklist built specifically for commercial brokers. It outlines what to prepare before going to market so buyers can evaluate the opportunity efficiently and move from interest to offer quickly.

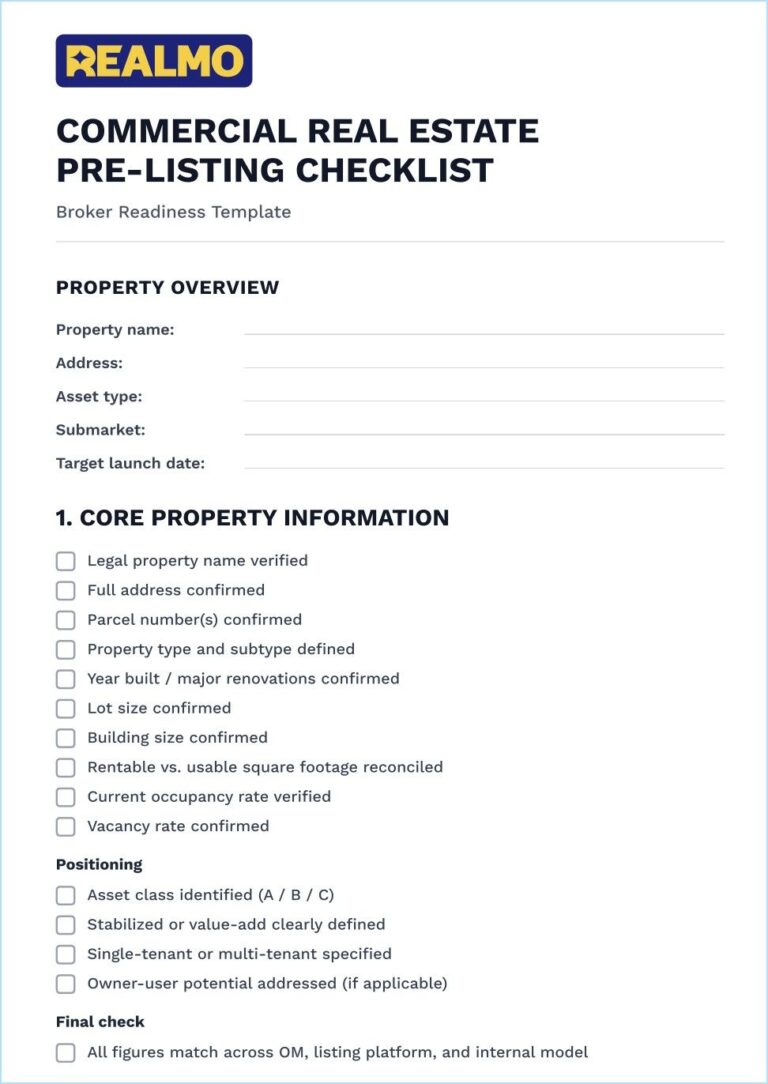

The Commercial Real Estate Pre-Listing Checklist

Preparation is one of the few variables fully within your control. Asset quality, capital flows, and interest rates will shift, but your standard for how a listing is assembled doesn’t have to.

Below is the complete checklist with examples, statistics, and extra tips for a better application. Each section reflects what serious buyers look for during underwriting and what typically slows deals when it’s missing.

1. Confirm core property information

Verify legal and physical basics:

- Full legal property name and address

- Parcel number(s)

- Property type and subtype

- Year built and major renovation dates

- Lot size and building size

- Rentable vs. usable square footage (consistent across all materials)

- Current occupancy and vacancy rate

Make sure the numbers align across every document. This includes offering memorandum, listing platform, and internal underwriting model. Inconsistent square footage or occupancy figures are one of the fastest ways to erode buyer trust.

Remember to clarify positioning, too:

- Asset class (Class A/B/C)

- Stabilized vs. value-add

- Single-tenant vs. multi-tenant

- Owner-user potential (if applicable)

If the opportunity requires explanation on a call, refine the description. A buyer should understand what they are looking at within the first page of the listing.

Pro tip: The easiest way to check this section is to review comparable active listings in the same submarket and asset class. See how similar properties are categorized and described. A good idea is to use a platform that combines listings and analytics in one place. You can try Realmo, a data-driven CRE marketplace with 1M+ nationwide listings and built-in analytics, which allows you to benchmark your positioning against live market inventory.

2. Prepare financial documents

Commercial transactions are income-driven. That’s why this section is so important. Here’s what you need to keep your eye on:

Organize the current performance:

- Clean rent roll (reconciled to reported income)

- Trailing 12-month income statement (T-12)

- Operating expense breakdown

- Net operating income calculation

- Vacancy assumptions clearly stated

All income figures should reconcile. If reported NOI differs from T-12 totals, explain why. Small discrepancies create unnecessary doubt.

Follow this up by clarifying the lease structure and risk:

- Lease start and end dates

- Escalation terms

- Expense reimbursement structure (NNN, gross, modified gross)

- Tenant concentration exposure

- Upcoming expirations

If rollover risk exists, address it proactively. Buyers will analyze it anyway.

It’s also a good idea to provide context for projections:

- Clearly separate actual income from pro forma assumptions

- State assumptions behind projected rent growth or stabilization

Pro tip: At this stage, avoid overly aggressive projections. Conservative, well-supported numbers are more credible than optimistic models that require explanation.

3. Validate pricing with market data

Before finalizing the asking price, understand where the asset sits relative to what buyers are actively evaluating. Study what is currently on the market in the same submarket and asset class. Buyers compare live opportunities first, then reference historical transactions.

Before publishing the asking price:

- Review recent comparable sales in the submarket

- Benchmark cap rates for similar asset types

- Analyze vacancy and absorption trends

- Assess supply pipeline and competing inventory

If your implied cap rate materially differs from recent transactions, be ready to explain why (location advantage, tenant quality, redevelopment upside, or lease term strength).

Pro tip: Take advantage of market analytics tools to automate the process. Use Realmo’s Analytics Center to analyze comparable transactions, benchmark cap rates within the submarket, and review current pricing trends before finalizing your asking price. Validating assumptions with live market analytics helps you position the asset based on data.

Simply enter the property address to generate accurate reports and calculations.

4. Review condition and compliance

Physical and regulatory risks can derail deals late in the process. Address them early.

Assess physical condition:

- Roof, HVAC, and major systems age

- Recent capital improvements

- Deferred maintenance items

- Structural or environmental concerns

If improvements are needed, disclose them in the listing. Surprises during inspection are far more damaging than transparent disclosures upfront.

Confirm regulatory standing:

- Zoning classification

- Permitted uses

- ADA compliance status

- Fire and safety compliance

- Environmental reports (Phase I/II, if applicable)

You don’t need to circulate full inspection reports or environmental studies in the initial marketing package. But before launching, confirm whether they exist, when they were last updated, and whether any material issues were identified. If a Phase I report is outdated or a roof inspection flagged repairs, know that in advance and decide how you’ll address it.

Transparency in this section prevents last-minute renegotiation.

5. Prepare professional marketing materials

Listings with professional-quality photos sell about 32% faster than those with amateur images. That’s just one illustration of how presentation influences perception, and perception shapes how quickly buyers engage. CRE is no exception here.

At the very least, prepare:

- High-resolution exterior and interior photography

- Clear floor plans or site plans

- A concise executive summary

- A structured offering memorandum

Your executive summary should answer:

- What is being sold?

- What is the income profile?

- What makes this opportunity distinct?

- Who is the ideal buyer?

Pro tip: Design the marketing package for scanning so that buyers can get a quick yet clear impression of the offer. Use simple, to-the-point headings, generous spacing, and consistent formatting. Keep text concise, break up content with tables and bullet points, and structure financials so key figures (NOI, cap rate, occupancy, lease terms) are visible at a glance.

6. Prepare for buyer due diligence

Roughly 50% of commercial real estate deals fall apart during due diligence. Reduce that risk by preparing early.

Before going live:

- Confirm all financials reconcile

- Ensure documentation is organized and accessible

- Identify any known risks or pending issues

- Decide what requires NDA before sharing

Think ahead to common buyer requests:

- Historical operating statements

- Service contracts

- Tax bills

- Insurance records

- Lease copies

You don’t need to distribute everything immediately, but you should know where it is and whether it’s complete. If discrepancies exist, address them proactively. For example, if income varies year over year, be ready to explain why. Or, if capital expenditures are planned, outline the scope and timeline.

Underwriting delays often begin with simple questions that could have been anticipated. The objective is straightforward: when a serious buyer requests diligence materials, you respond confidently and quickly.

7. Do a final review before launch

Before publishing the listing:

- Read the offering memorandum start to finish

- Confirm numbers match across all materials

- Validate that pricing logic is consistent

- Remove ambiguous statements

Ask one final question: Can a buyer understand this asset without a follow-up call?

If the answer is yes, the property is ready. If not, keep refining.

How to Use This Checklist Before You Go to Market

Incorporate this checklist before you set a launch date and treat it as a readiness filter. Here’s how you can apply it:

1. Adjust the checklist by asset type

The core checklist applies to all commercial properties. But buyers underwrite different asset classes differently. Adjust your emphasis depending on what you’re bringing to market.

Multifamily

Buyers will focus on income durability and expense efficiency.

Here are the core aspects worth highlighting:

- Lease expiration clustering and renewal history

- Unit mix and rent comparables

- Operating expense ratio versus submarket averages

- Any value-add assumptions tied to renovation or rent lift

If you’re projecting rent growth, support it with recent lease comps.

Industrial

For industrial assets, lease structure and tenant credit matter more than finishes. Emphasize the following:

- Remaining lease term

- Tenant credit quality

- Rent escalations

- Clear height, loading configuration, and building functionality

If there is near-term rollover, clarify whether the space is easily releasable in the current market.

Retail

Retail buyers will underwrite traffic, co-tenancy, and tenant stability. Be clear about:

- Anchor tenant strength

- Co-tenancy clauses

- Sales performance (if available)

- Surrounding traffic drivers and demographics

Remember that vacancy in retail requires context: is it location-driven, tenant-specific, or part of a broader market shift?

Office

Office underwriting is highly sensitive to rollover risk and capital exposure. Address directly:

- Lease expiration schedule

- Tenant improvement obligations

- Leasing commissions exposure

- Sublease competition in the submarket

If the asset requires repositioning, define the strategy clearly. Ambiguity around future leasing is where pricing discussions widen.

2. Review it in one focused pass

Don’t complete the checklist gradually over several days. Set aside a focused working session and go through it, start to finish.

Seeing every section at once helps you spot inconsistencies, weak assumptions, and areas that feel underdeveloped right away. When preparation is fragmented, gaps are easy to miss.

Example: You might notice that projected NOI assumes stabilized occupancy, while the rent roll shows several near-term expirations. In that case, you would either adjust the underwriting to reflect rollover risk more conservatively or clearly explain the leasing strategy in the offering memorandum, including renewal history, tenant quality, or active negotiations. The point is to reconcile the narrative with the numbers before the buyer does.

3. Separate confirmed data from assumptions

As you complete the checklist, distinguish clearly between verified numbers and projections. If something is estimated, whether related to income, expenses, or future upside, label it as such. This prevents confusion later and avoids unnecessary clarification during buyer conversations.

Before publishing the listing:

- Confirm recent comparable transactions

- Benchmark cap rates in the submarket

- Review current vacancy and absorption trends

- Stress-test projected income assumptions

If pricing cannot be clearly supported with data, adjust it before going live. Market-backed validation tools can help you ground your pricing in current analytics rather than historical assumptions.

4. Stress-test the listing from a buyer’s perspective

Before you publish the listing, step out of the broker mode and into the buyer mode. Ask yourself three key questions:

- If I saw this listing for the first time, what would I question?

- What assumptions would I want verified?

- What information would I need before seriously underwriting?

If parts of the listing rely on explanation during a call, they’re not ready. The same is true if buyers need multiple follow-ups to understand the opportunity.

Example: If the listing highlights stable income, but the rent roll shows that 40% of leases expire within the next 18 months, a buyer will immediately question how stable that income really is. Before going live, you would either adjust the positioning to acknowledge the rollover exposure or clearly explain the renewal history and leasing strategy. Addressing that mismatch upfront keeps the narrative consistent and prevents the buyer from controlling the conversation later.

5. Make it a standard

Use the same preparation standard for every listing, regardless of asset size. It creates a simple chain reaction:

| Consistency builds discipline → Discipline reduces errors → Buyers know what to expect from your listings |

Over time, that predictability shortens initial review cycles, reduces clarification emails, and builds credibility with repeat buyers. When investors recognize that your listings are structured and complete, they approach new opportunities with fewer reservations.

Download the Commercial Real Estate Pre-Listing Checklist (Free PDF)

Download the free checklist template here

Why Many Commercial Listings Take Too Long to Sell

Most commercial listings take a while to sell because buyers are pricing risk more aggressively than they did just a couple of years ago.

Commercial real estate has gone through a major repricing cycle. According to J.P. Morgan, property values fell roughly 25% from their 2022 peak, even though net operating income continued to grow. In other words, assets didn’t necessarily perform worse, but buyers and investors became more cautious.

That’s why people tend to move forward only when they have clarity. If financials are incomplete, pricing is weakly supported, or documentation is missing, underwriting slows down. Momentum is often lost, which extends time on market.

Why listing quality might be part of the problem

The logic is pretty simple: if buyers are pricing risk more aggressively, then anything that increases uncertainty will slow a deal down.

In these scenarios, listing quality can become a decisive factor, and it often does. A property can stay on the market because buyers cannot evaluate it with confidence, although the demand may be high.

And if residential buyers can act on emotion, commercial buyers are way less impressionable. They are underwriting income streams, reviewing lease terms, assessing rollover exposure, and validating assumptions against submarket data. If that information isn’t clearly structured within the listing package, buyers have to reconstruct it themselves. And no one wants to do the extra work they’re not supposed to do.

Common listing-related issues that delay transactions include:

- Rent rolls that don’t reconcile with reported income

- Missing or outdated T-12 financials

- Inconsistent square footage across documents

- Pricing that is not supported by current comps or cap rate benchmarks

- No clear disclosure of capital expenditures or deferred maintenance

None of these issues automatically makes the asset unattractive. But in a market full of cautious buyers, they amplify perceived risk, and this is never good news for the broker. Perceived risk makes buyers take longer to submit offers, negotiations become more defensive, and capital can simply move to a competing listing that feels easier to evaluate.

How a Complete Listing Can Help You Sell Faster

A complete listing makes decision-making faster. Buyers and investors focus on evaluating the opportunity itself instead of requesting missing documents, reconciling inconsistent numbers, or challenging unsupported assumptions.

The impact shows up in three ways:

- Faster initial engagement. Serious buyers can assess fit quickly and decide whether to pursue the asset without delay.

- Shorter underwriting cycles. Clean rent rolls, organized expense data, and accessible documentation reduce back-and-forth communication.

- Stronger competitive tension. When multiple buyers can underwrite confidently at the same time, offers tend to arrive closer together, which protects pricing and negotiation leverage.

Combine all three, and you get a smoother transaction process since the property attracts serious offers faster.

Final Word

Buyers and investors are getting faster at filtering opportunities and less tolerant of ambiguity. Listings that require explanation don’t get the benefit of the doubt but simply get skipped.

This checklist template helps you treat listings as structured data packages rather than marketing brochures. Once your listing allows a buyer to underwrite confidently, you’ll feel the difference immediately in the quality of conversations that follow.